Data centers are being used to store information by companies from all industry sectors. Companies need reliable places to store data, and that’s where enterprise data centers come in. These data centers are established by companies themselves to store information. Besides enterprise data centers, there are internet data centers and third party operators. Internet data centers store high amounts of data from the cloud which require comparatively more servers, equipment, and power. Third party operators construct facilities and provide services for enterprise and internet data centers.

There are a number of requirements for data centers to function. They need telecommunications equipment, semiconductors, wirings and cables, power conversion equipment, and more. Data centers consume large amounts of energy. A single data center is known to have consumed enough energy required to run a small town. Google Inc., in 2013, had 13 data centers all over the world which used around 260 million watts of power which accounts to 0.01% of global energy. That amount of power can supply electricity to 200,000 homes. Data centers also need to be secured and running 24 hours a day. A typical data center needs multiple sources of power backup. They also need a good source of cooling. HVAC equipment manufacturers provide data centers with cooling units and heat exchangers.

Technologies in computing systems determine the lifespan of data centers. The average life span of a data center is estimated to be around 8-10 years because of the evolving technology. When we look at current technology trends in data centers, cloud computing is gaining popularity among service providers. Equinix a company which provides services for companies like Amazon, Microsoft, IBM and Cisco, says that its cloud platform has more opportunities to grow as companies are switching from enterprise data centers to the cloud.

Automated network management systems are emerging in the data center market as well. Recently, Wave2Wave, a Silicon Valley-based company, designed robotic network switches for data centers and telecommunications facilities which operate physical network configuration, plugging and unplugging physical ports on command from software, allowing physical data center network connections to be managed quickly and remotely. Although automation in network management has been a trend in recent years, the previous systems ran on physical switches, servers, and routers, linked by physical network cables, and plugging and unplugging network cables had been the physical limit to how far automatic network configuration could have gone. Innovation has also taken place in data center security. Facebook designed a system called NetNORAD which constantly monitors all of Facebook data center infrastructure for packet loss rates and latency. Using data analytics, it detects abnormal patterns and triggers alarms, usually within 30 second of a fault. Facebook also open sourced some of the software tools it had built in-house that help its engineers detect the location of an outage within its infrastructure down to a single cluster of servers within a matter of seconds, isolate the fault, and avoid a wider-scale issue.

Operating a data center requires a minimum investment of $50 million, and investments can reach up to $1 billion or more depending on the type of infrastructure. A recent study conducted by International Data Corporation (IDC) found that North America will provide the largest share of global IT spending throughout the 2015-2019 forecast period which is forecasted to pass the $1 trillion mark in 2017. Even though a data center typically only employs 10 to 30 people, indirect employment from data centers is massive if we look at the total employment created by equipment manufacturers for data centers.

According to a recent JLL report, in 2015 the data center market in North America saw growth of 6.1 percent with providers in the U.S. earning revenues of $115.6 billion. The study found that Northern Virginia had a year-to-date absorption of 63 MW followed by Dallas with 42.3 MW and Seattle and Portland with 39 MW YTD absorption in 2015. Data center operators and service providers are looking for accessible markets which are secure and cost effective. As prices grow, companies are targeting emerging market areas.

In a 2014 report published by CBRE, it was found that the most attractive data center leasing spaces in the U.S. based on lease costs, power costs, sales taxes, property taxes and potential incentives, were Atlanta, Colorado Springs, Northern Virginia, Portland, and Seattle.

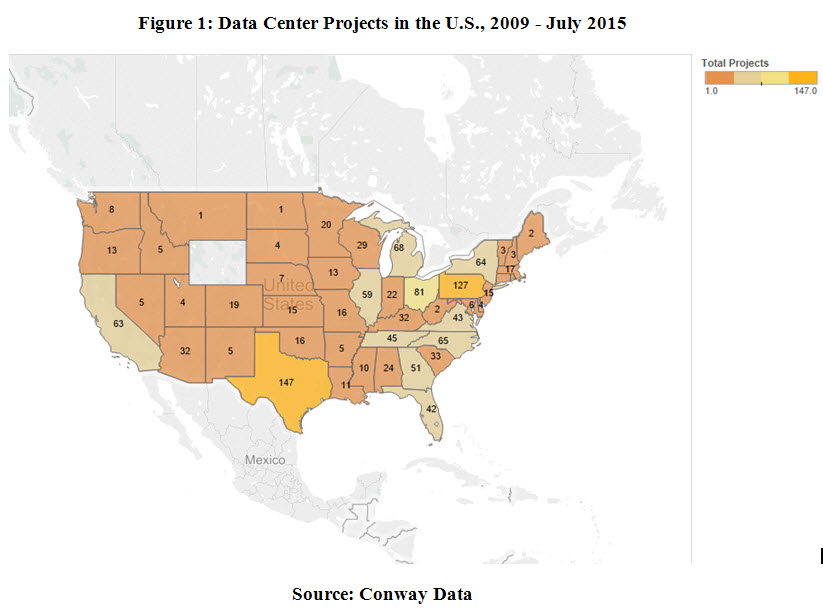

If we look at data from Conway, there have been a total of 1267 projects from data center service providers from 2009 to July 2015 . Out of the announced 1267 projects, 602 were new and 665 were expansion projects. Texas is at the top with a total of 147 projects, followed by Pennsylvania with 127 and Virginia with 81 projects.

In Texas, Facebook started construction on a 750,000 square foot facility in Fort Worth in July 2015, investing almost $1 billion. HP has several data centers in Texas, and recently it signed a 12-year contract to buy 112 megawatts of wind power from a SunEdison wind farm in Texas. Texas has attracted high amounts of investments from data centers as well as service providers. In Houston, demand is driven by oil and gas companies. Data centers are providing energy companies with space to store drilling and exploration information. Houston also has a big community of healthcare organizations.

In Pennsylvania, TierPoint, a cloud, colocation, and managed services provider finished an expansion project increasing the available space by 150 percent. US Utility announced the construction of a new data center, and Data Based Systems International (DBSi) launched a new facility in June 2011. Pennsylvania seems to be targeting data center growth. In July 2015, Pennsylvania proposed to start offering tax breaks to data centers. If approved, data centers could save up to 8 percent in running costs.

Virginia has become one of the top markets for data centers. It was predicted by 451 Research, in 2015, that Northern Virginia would overtake New York Metro as the biggest multi-tenant data center market. Northern Virginia was made for data centers, with abundant fiber, cheap and reliable power from Dominion Virginia, and attractive tax incentive programs.

A recent noteworthy announcement in Michigan is the new $5 billion Switch data center that is being constructed just outside Grand Rapids. It is expected to bring 1,000 new jobs to the area over the next decade.

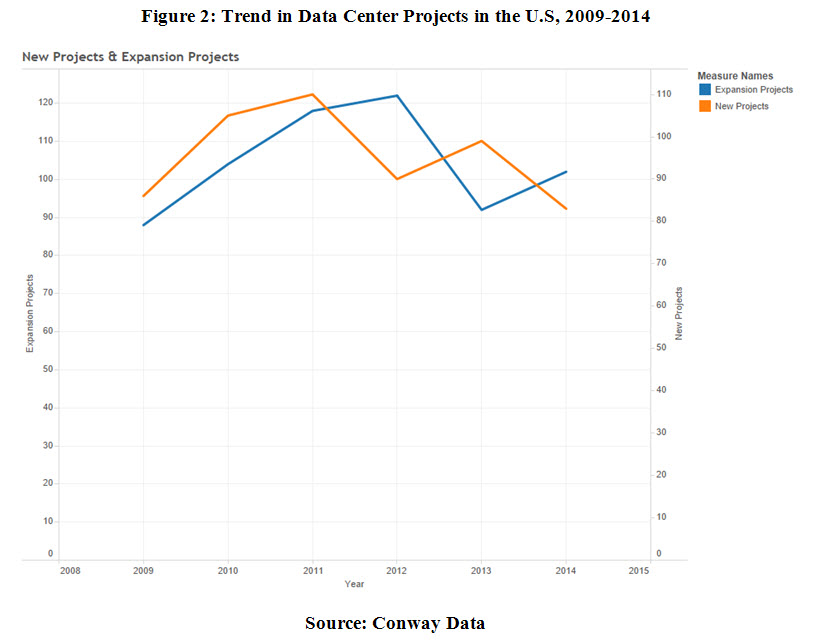

When we look at the trend in projects from 2009 to 2014, what started out as an increase for the first two years in both new and expansion projects has decreased over the past 3 years. The year 2011 had the highest number of projects with 228 total projects consisting of 118 expansion and 110 new projects while 2009 was the lowest for projects with 174 total projects.

Top infrastructure providers are doing business in America. ABB Ltd., an electric equipment manufacturer based in Switzerland that provides power protection and conditioning solutions, including DCIM software and modular UPS solutions to data centers, has had numerous new and expansion projects in recent years. In 2014, the company established a new facility in Wisconsin for producing service center drives, low voltage products, and power electronics. The company also won several contracts in the U.S. over the years. Asetek is one of the top manufacturers of liquid cooling systems for data centers. The company has been awarded several contracts in recent years from computer manufacturers to data centers. EdgeConneX, Inc. a company which provides infrastructure solutions for content providers, network and cable operators, and colocation companies, announced three new projects in Florida. The company also announced a new facility in Minnesota.

Since there are so many industry sectors involved, it shows that providing services for data centers is big business. Data centers alone bring large investments to the community. When service providers step in, it is an added bonus for developers. Data centers look for affordable areas with good options in services. An area is most likely to get data center investment if there is an option to choose from services, and these service providers are most likely to establish facilities in the same areas as data centers. Economic development agencies should look at these factors to utilize opportunities provided by both data centers and their service providers.